More and more cities in California are developing Climate Action Plans (CAPs). During our climate action planning work with cities, we repeatedly hear questions from the public and city staff about costs. How much is this climate action plan going to cost the city, and by extension taxpayers? Which measures get us the biggest emissions bang for our buck? What’s the bottom line? What are the financial impacts to homeowners and businesses? These questions have merit—after all, it is important to understand who will be financially impacted by a city’s policies and actions. In response, the Energy Policy Initiatives Center (EPIC), in partnership with the San Diego Association of Government’s Energy Roadmap Program, has developed a method for evaluating the cost implications of CAPs. This post, the first in a series to describe these methods, summarizes the basics of CAP cost analyses and provides context for the material covered in future posts.

Goal of CAP Cost Analyses

We have learned that, in general, the goal of CAP cost analyses is to answer three questions:

- What are the costs to a local jurisdiction to implement a CAP?

- How cost-effective are CAP measures at reducing greenhouse gases (GHGs)?

- What are the financial impacts to those who participate in CAP measure activities?

Two separate analyses are used to answer these questions: an implementation cost analysis (ICA) answers the first question and a benefit-cost analysis (BCA) answers the last two. While the ICA and BCA are separate in scope, they are interconnected; data gathered for the ICA are used to inform part of the BCA.

The purpose of these analyses is to inform decision-makers, local jurisdiction staff, residents, businesses, and all other potential stakeholders who have an interest a city’s CAP. Cost analyses can occur at several stages during the climate action planning cycle (checkmarks, Figure 1). During earlier stages (estimating GHG reductions and CAP development), cost analyses can aid in the CAP measure selection process. If conducted during implementation, results can help prioritize actions or help identify ways to more efficiently spend city funds. During later stages of the cycle (monitoring & reporting and CAP updates), analyses can integrate ex post data to better understand actual impacts since CAP adoption and tailor strategies going forward as necessary.

Figure 1. Climate Action Planning Cycle

Cost is but One Piece of the CAP Puzzle

Before jumping into further detail, it is important to recognize the role of cost analyses in the CAP process. In general, results from cost analyses are used to evaluate GHG reduction measures included in or being considered in a CAP. While cost is an important consideration, results should be viewed in a broader context. For example, when selecting GHG reduction measures, there are many other factors to consider (Figure 2). Focusing too narrowly on cost analyses during the decision-making process may lead to a tendency to prioritize CAP measures with the best cost profile, without little understanding of the strategy’s feasibility or potential to reduce emissions.

Figure 2. Select Considerations for Analyzing CAP Measures

Implementation Cost Analysis

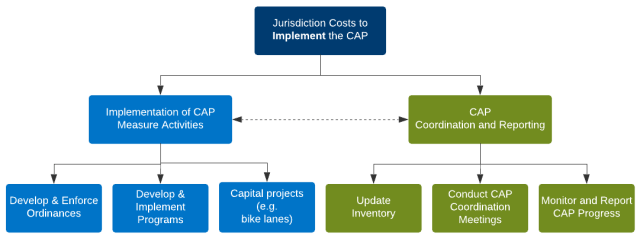

A CAP ICA answers the question: What are the costs to a jurisdiction to implement a CAP? The ICA analyzes the costs incurred by the jurisdiction to implement the CAP, including costs directly associated with activities identified in CAP measures (Figure 3, blue boxes) and costs associated with overall CAP coordination and reporting (Figure 3, green boxes).

Figure 3. Costs Included in a CAP Implementation Cost Analysis

In general, ICAs align with a jurisdiction’s budgeting cycle and analyze only the first several years of CAP implementation (e.g., 5–6 years). Estimates that expand past the budgeting horizon are often highly speculative and uncertain.

An ICA can differentiate between total and incremental costs or a new and existing program. Costs can be broken down by CAP measure, department, and/or activity type. The level of detail included in the ICA can vary according to a jurisdiction’s needs and staff availability.

Benefit-Cost Analysis

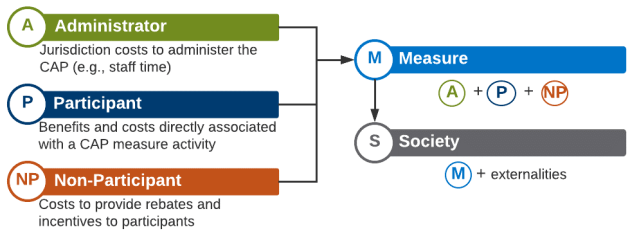

A CAP BCA answers the questions: How cost-effective are CAP measures at reducing GHGs and What are the financial impacts to those who participate in CAP measure activities? The BCA incorporates the benefits received and costs incurred across five perspectives (Figure 4)—a framework that has been adapted from the CPUC’s Standard Practice Manual to apply specifically to CAPs.

Figure 4. CAP Benefit-Cost Analysis Perspectives

The Administrator perspective includes the jurisdiction’s costs to implement and administer a CAP measure. The Participant perspective includes the costs and benefits of those directly involved in a CAP measure activity (e.g., homeowners, business, and possibly the jurisdiction itself). The Non-participant perspective accounts for the costs associated with funding subsidies (e.g., rebates, incentives, tax credits, etc.) that offset some of the costs incurred by Participants. The Measure perspective aggregates the first three perspective and provides a more holistic view of the direct benefits and costs associated with a CAP measure. Lastly, the Societal perspective integrates positive and negative externalities to the Measure perspective.

A CAP BCA is designed to align with GHG estimates used in CAP calculations and results capture the estimated impacts of all activity necessary to achieve GHG reductions in specific target years. Several common benefit-cost analysis metrics are calculated to assess measure cost-effectiveness and impacts on participants (Figure 5).

Figure 5. CAP Benefit-Cost Analysis Metrics

What’s coming up next?

This was the first in a series of posts about CAP cost analyses. Our next post will dive deeper into a CAP ICA and later posts will continue to explore methods and concepts included in a CAP BCA. The series will conclude with a discussion highlighting some of the current challenges and limitations faced in developing CAP cost analyses.

Pingback: The Cost of a CAP Part 2: How Much is This Climate Action Plan Going to Cost Our City? | The EPIC Energy Blog

Pingback: The Cost of a CAP Part 3: The Benefits and Costs of CAP Measures | The EPIC Energy Blog

Pingback: The Cost of a CAP Part 4: Emissions Bang for Your Buck | The EPIC Energy Blog

Pingback: The Cost of a CAP Part 6: Limitations | The EPIC Energy Blog

Thannk you for sharing this