More and more, local jurisdiction staff, decision makers, and stakeholders are interested in the cost of implementing climate action plan measures and actions. We are often asked by local jurisdiction officials some form of the question: how much is thing going to cost us? The first post in this series by EPIC Technical Policy Analyst Marc Steele presented an overall summary of climate action plan (CAP) cost analyses and outlined three questions we are trying to answer. This post focuses on the implementation costs analysis (ICA), which answers the first of those questions: What is the budgetary impact to a local jurisdiction to implement CAP measures? It begins by defining the ICA and then discusses the types of costs evaluated, when an ICA can occur in the climate planning process, and considerations for evaluating CAP implementation costs.

What is a CAP Implementation Cost Analysis?

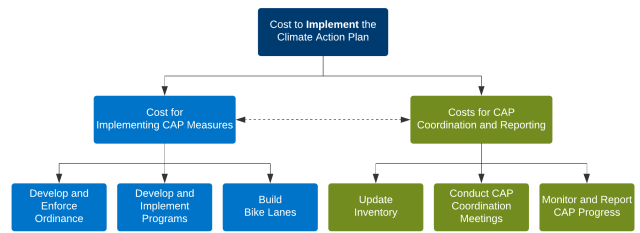

A CAP ICA estimates costs incurred by the local jurisdiction to implement measures and associated activities in a CAP. It is basically an evaluation to assess the impact that implementing CAP activities will have on the budget and resources of a local jurisdiction. An ICA considers costs associated with two broad categories of CAP implementation: (1) activities directly related to CAP measures and (2) overall CAP coordination and reporting. The first category includes activities to develop and implement CAP measures, such as developing ordinances, developing programs, conducting education and outreach, conducting energy or water saving projects in local jurisdiction facilities, and building bike lanes (Figure 1, blue boxes). The second category of activities includes regularly conducting GHG inventories to track progress, regularly reporting CAP progress, and coordinating internal activities among departments (Figure 1, green boxes).

Figure 1. General Cost Types Included in Implementation Cost Analyses

When to Conduct CAP Implementation Cost Analyses

Figure 2 presents the overall climate action planning cycle. A local jurisdiction can develop an ICA at several steps in the climate action planning process. During the CAP development process, local jurisdictions typically develop a list of potential GHG reduction measures to be evaluated for inclusion in the CAP. Understanding the cost to a local jurisdiction to implement a CAP measure can help inform this evaluation.

If a detailed estimate of CAP implementation costs is not completed or included in the CAP document, the analysis can be completed at the time a local jurisdiction develops a standalone CAP implementation plan. Most CAPs include a section on implementation, but more detailed and specific implementation plans are generally developed after the CAP is adopted. Similar to considering cost at the point of selecting GHG reduction measures to include in the CAP, conducting a cost analysis for an implementation plan provides results that can be considered with a range of other variables to help decision-makers and staff prioritize when measures are implemented.

Many CAPs include requirements to regularly monitor and report on the progress of measure implementation and emissions reductions. At this point in the climate action planning cycle, local jurisdictions could evaluate numerous aspects of the CAP to determine progress, including overall emissions, emissions by sector, performance metrics associated with specific measures and actions, and whether supporting activities have been completed. An ICA would help a local jurisdiction understand the cost and level of staffing that has been committed to CAP implementation and its effect on internal operations.

In addition to monitoring, some CAPs also call for regular CAP updates. Conducting an ICA at this point in the climate action planning cycle is similar to that during the CAP development process. ICA results can help inform decision-makers on new or updated measures being considered for the updated CAP.

Figure 2. Climate Action Planning Cycle

Implementation Cost Analysis Process

The goal of a CAP ICA is to estimate the cost of implementing activities called for in CAP measures and actions. The general steps in the process are to identify and estimate the following: anticipated tasks required to implement CAP actions; staffing needs to complete the required tasks; non-staffing needs; staffing costs; and non-staffing costs, including capital, consultant, and supply and material expenditures (Figure 3). This data-driven process is based on inputs and estimates provided by local jurisdiction staff. As a result, staff time needed to complete the data collection process is a factor for local jurisdictions.

Figure 3. Process to Develop CAP Implementation Costs

Which CAP Implementation Costs to Include

The type and number of costs evaluated in an ICA depend on the goals of the analysis. For example, if a local jurisdiction is mostly concerned with the staffing impacts of implementing CAP measures, then focusing only on salary and benefit costs would be sufficient. If a local jurisdiction wanted to know the total cost to implement a CAP, then evaluating all expenditure categories would yield a more complete estimate. Local staff typically develop the necessary data to evaluate CAP implementation costs. In general, the broader the scope of the analysis—that is, the more expenditure categories that are considered—the higher the level of staff involvement required.

Expenditure Categories

The expenditure categories used to collect and analyze cost data can be determined by local jurisdiction preferences and general budgeting conventions. While each local jurisdiction may have its own expenditure categories and system of grouping expenditures, the following are typical.

- Capital – Capital expenditures by local jurisdictions are typically for projects and programs related to local jurisdictional operations, such as installing solar photovoltaics (PV) on municipal facilities, but also can include public works projects that affect the broader community, such as bike lane construction.

- Salary and Benefits – This category represents the personnel costs to implement CAP activities. Salary and benefit costs are calculated using estimated hours for each staff position that would be required to implement CAP activities and the fully-burdened hourly rate, which typically includes current base salary, benefits (e.g., healthcare and retirement), and any other associated overhead costs. In addition to the staffing cost, it is possible to examine the staffing impacts (full-time equivalent (FTE)) that would result from the anticipated tasks related to each CAP measure.

- Consultants – Local jurisdictions often hire external consultants to support CAP implementation activities, including to develop ordinances, prepare environmental impact reports (EIRs) under the California Environmental Quality Act (CEQA), conduct transportation demand studies, and analyze emissions and CAP progress to regularly monitor and report CAP progress.

- Materials & Supplies – Many CAP activities require materials and supplies. These can include brochures and meeting materials for outreach activities.

Considerations for Evaluating CAP Implementation Costs

There are numerous considerations to analyze the costs associated with CAP implementation programs and activities, including the following.

- Program Status – This helps to distinguish between CAP programs that already exist or that will be part of an expanded or new effort. This can be a necessary step to identify the incremental costs due to CAP implementation.

- Funding Status – Identifying whether CAP activities are already funded or if additional funding would be necessary can help to identify the incremental funding that would be needed to implement the CAP. Existing programs that are already funded, would have no impact on a local jurisdiction’s budget.

- Position Status – Determining whether positions identified as necessary to implement CAP activities would be existing or new can help a local government gauge the staffing levels that would be required to implement CAP activities.

- Funding Source – Identifying whether or not funding sources exist for the level of effort necessary to implement CAP activities can help the internal budgeting process.

- Timeframe of Analysis – Local governments can determine how many years to capture in an ICA. Generally, local governments evaluate the first 5 years. This can align with existing budget timeframes.

Total or Incremental Activity Costs

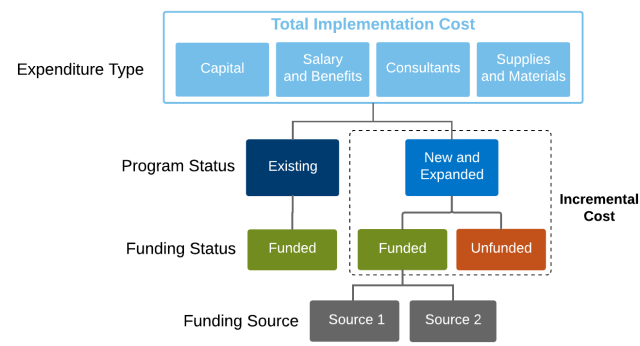

A CAP ICA can estimate total costs, incremental costs, or both. As described above, whether an activity and its associated cost is incremental to the CAP is a function of program status. Total cost is determined by summing the cost of all activities by expenditure type. The proportion of the total activity that is associated with the new activities and the expanded portion of existing activities is considered incremental (Figure 4). Incremental activity costs can comprise funded and unfunded activities; this represents the total cost to implement activities that would not have occurred without CAP adoption. Costs associated with unfunded incremental activities in this example (orange box) represent the amount of additional funding that would be necessary to complete activities that would only be undertaken because of the CAP. This amount could be referred to as the “incremental budget impact” of the CAP.

Figure 4. Framework for Determining Incremental Costs

Examples of CAP Implementation Cost Analyses

EPIC has completed several implementation cost analysis for local jurisdictions in the San Diego region that follow the framework presented here, including County of San Diego and City of La Mesa (Appendix D).

In Part 3 of this series, EPIC Technical Policy Analyst Marc Steele will continue the discussion on CAP cost analyses and present a framework for conducting benefit-cost analyses for CAPs.

Pingback: The Cost of a CAP Part 3: The Benefits and Costs of CAP Measures | The EPIC Energy Blog

Pingback: The Cost of a CAP Part 6: Limitations | The EPIC Energy Blog